Income Tax Rules 2026

Income Tax Rules 2026

New Income Tax Rules 2026

Income-tax Rules, 2026 These will come into effect on April 1, 2026.

Navin Praptikar Kayda 2026

नवीन प्राप्ती कर कायदा २०२६, १ एप्रिल २०२६ पासून अंमलात येतील.

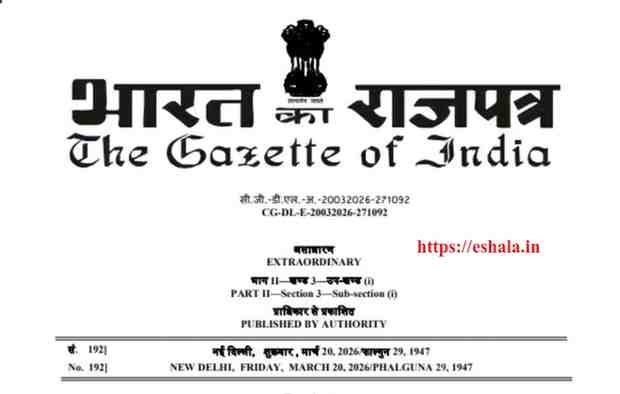

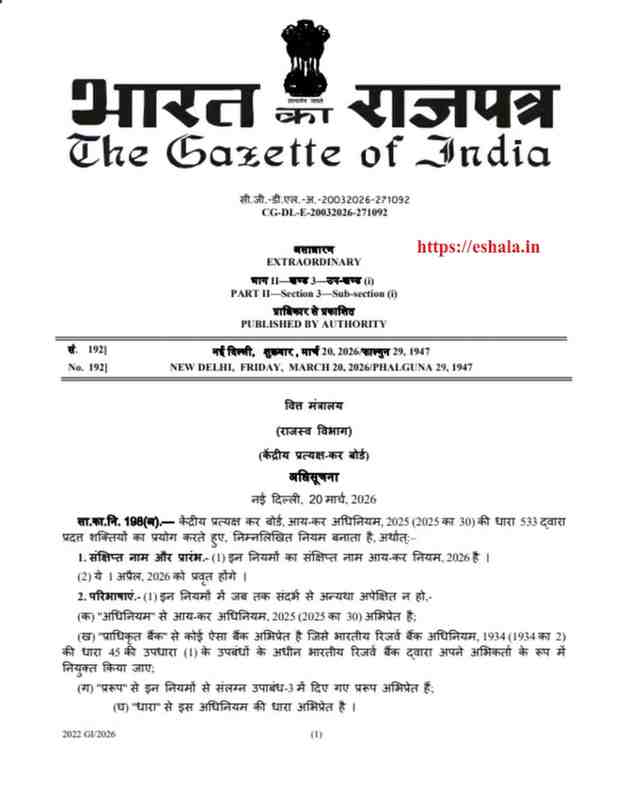

भारत का राजपत्र

The Gazette of India

सी.जी. डी.एल. अ.-20032026-271092 CG-DL-E-20032026-271092

असाधारण EXTRAORDINARY

भाग 11-खण्ड उप-खण्ड (1) PART II-Section 3-Sub-section (i)

प्राधिकार से प्रकाशित PUBLISHED BY AUTHORITY

चं. 192

नई दिल्ली, शुक्रवार, मार्च 20, 2026/फाल्गुन 29, 1947

No. 1921

NEW DELHI, FRIDAY, MARCH 20, 2026/PHALGUNA 29, 1947

वित्त मंत्रालय (राजस्व विभाग) (केंद्रीय प्रत्यक्ष कर बोर्ड)

अधिसूचना

नई दिल्ली, 20 मार्च, 2026सा.का.नि. 198 (ब).- केंद्रीय प्रत्यक्ष कर बोर्ड, आय-कर अधिनियम, 2025 (2025 का 30) की धारा 533 द्वारा प्रदत्त शक्तियों का प्रयोग करते हुए, निम्नलिखित नियम बनाता है, अर्थात्ः-

- संक्षिप्त नाम और प्रारंभ. (1) इन नियमों का संक्षिप्त नाम आय-कर नियम, 2026 है।

(2) ये 1 अप्रैल, 2026 को प्रवृत होंगे ।

- परिभाषाएं.- (1) इन नियमों में जब तक संदर्भ से अन्यथा अपेक्षित न हो.-

(क) “अधिनियम” से आय-कर अधिनियम, 2025 (2025 का 30) अभिप्रेत है;

(ख) “प्राधिकृत बैंक” से कोई ऐसा बैंक अभिप्रेत है जिसे भारतीय रिजर्व बैंक अधिनियम, 1934 (1934 का 2) की धारा 45 की उपधारा (1) के उपबंधों के अधीन भारतीय रिजर्व बैंक द्वारा अपने अभिकर्ता के रूप में नियुक्त किया जाए;

(ग) “प्ररूप” से इन नियमों से संलग्न उपाबंध-3 में दिए गए प्ररूप अभिप्रेत हैं;

(घ) “धारा” से इस अधिनियम की धारा अभिप्रेत है।

KIND ATTENTION TAXPAYERS!

Income-tax Rules, 2026 have been notified and published in the e-Gazette.

The notification may be accessed on:

ALSO READ –

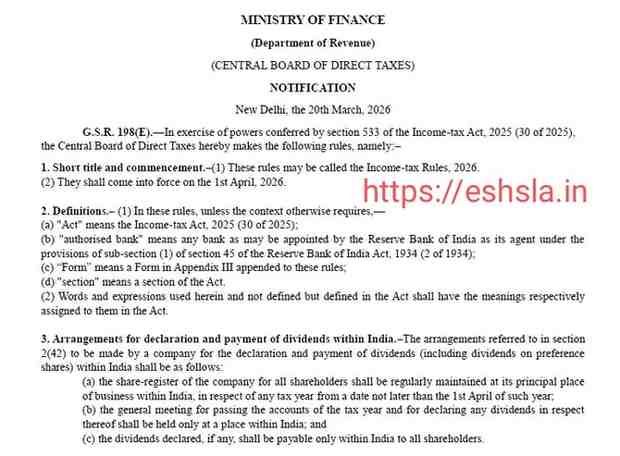

MINISTRY OF FINANCE

(Department of Revenue)

(CENTRAL BOARD OF DIRECT TAXES)

NOTIFICATION

New Delhi, the 20th March, 2026

G.S.R. 198(E). In exercise of powers conferred by section 533 of the Income-tax Act, 2025 (30 of 2025), the Central Board of Direct Taxes hereby makes the following rules, namely:-

1. Short title and commencement.-(1) These rules may be called the Income-tax Rules, 2026.

(2) They shall come into force on the 1st April, 2026.

2. Definitions.- (1) In these rules, unless the context otherwise requires,-

(a) “Act” means the Income-tax Act, 2025 (30 of 2025);

(b) “authorised bank” means any bank as may be appointed by the Reserve Bank of India as its agent under the provisions of sub-section (1) of section 45 of the Reserve Bank of India Act, 1934 (2 of 1934);

(c) “Form” means a Form in Appendix III appended to these rules;

(d) “section” means a section of the Act.

(2) Words and expressions used herein and not defined but defined in the Act shall have the meanings respectively assigned to them in the Act.

3. Arrangements for declaration and payment of dividends within India. The arrangements referred to in section 2(42) to be made by a company for the declaration and payment of dividends (including dividends on preference shares) within India shall be as follows:

(a) the share-register of the company for all shareholders shall be regularly maintained at its principal place of business within India, in respect of any tax year from a date not later than the 1st April of such year,

(b) the general meeting for passing the accounts of the tax year and for declaring any dividends in respect thereof shall be held only at a place within India, and

(c) the dividends declared, if any, shall be payable only within India to all shareholders.